Bitcoin-backed lender comparison summary

This guide compares eight bitcoin-backed lending platforms available to US borrowers in 2026 (Strike, Coinbase, Nexo, SALT, Ledn, Figure, Unchained, and Arch) and evaluates rates, fees, custody, liquidation policy, and availability. APRs range from roughly 5% to over 14%, with most platforms between 8% and 13%. Origination fees range from 0% to 2%. Custody models span traditional custodians, collaborative multisig, and on-chain smart contracts. Some platforms perform partial liquidations while others liquidate the entire position. Most offer fixed-term loans, and a few offer revolving credit.

The bitcoin-backed lending market in 2026

Bitcoin holders face a recurring tension. They want to keep their bitcoin but also need cash for bills, down payments, business expenses, and other short-term obligations. Selling creates a taxable event and gives up future price exposure. Borrowing against bitcoin solves both problems.

The bitcoin-backed lending market looks very different from what it did a few years ago. Today, US customers can choose from homegrown Bitcoin-only companies, global multi-asset platforms, and even on-chain protocols routed through major exchanges. Each comes with trade-offs in cost, custody, flexibility, and regulatory oversight.

This guide evaluates eight platforms across the dimensions that matter most to a US-based borrower.

Bitcoin-backed lending rates, fees, and terms compared

| Strike | Coinbase | Nexo | SALT | Ledn | Figure | Unchained | Arch | |

|---|---|---|---|---|---|---|---|---|

| Loan term | 1 year or revolving | Revolving | Revolving | 1, 3, or 5 years | 1 year | 1 year | 1 year | 1 year |

| Collateral | BTC | cbBTC | BTC and altcoins | BTC and altcoins | BTC | BTC and altcoins | BTC | BTC and altcoins |

| Max initial LTV | 50% | ~75% | 50% | 70% | 50% | 75% | 50% | 60% |

| APR1 | 7.75%–13% | ~5% | 1.9%–17.9% | 9.95%–14.45% | 9.75%–10.99% | 10%–12.62% | 14.18% | 7.25%–10.99% |

| Origination fee | 0% | 0% | 0% | 1% | 0% | 1% | 2% | 1.49% |

| Liquidation fee | 0% | ~5% | 2% | 3%–5% | 0% | 2% | 2% | 2% |

| Liquidation type | Partial | Full | Partial | Partial | Full | Partial | Full | Partial |

| Collateral retrieval | Yes | No | Yes | Yes | Yes | No | No | Yes |

| Minimum loan | Starts at $5,000 | No stated minimum | $50 | $5,000 | $500 | $5,000 | $150,000 | $1,000 |

| Eligible borrowers | Individuals and businesses | Individuals | Individuals and businesses | Individuals and businesses | Individuals | Individuals | Businesses | Individuals and businesses |

| US availability | 50 states + D.C. + P.R. | 49 states | TBA | 50 states + D.C. | 40 states | 40 states | 42 states | 35 states |

| Lending-only | No | No | No | Yes | No | Yes | No | Yes |

1 For platforms that charge an origination fee, the APR includes that fee. APR ranges vary by platform. Strike, Ledn, and Arch are tiered by loan size. SALT and Figure vary by LTV and loan term. Coinbase's rate is variable, set algorithmically based on real-time pool utilization. Nexo's rate depends on the borrower's loyalty tier, determined by NEXO token holdings as a percentage of portfolio.

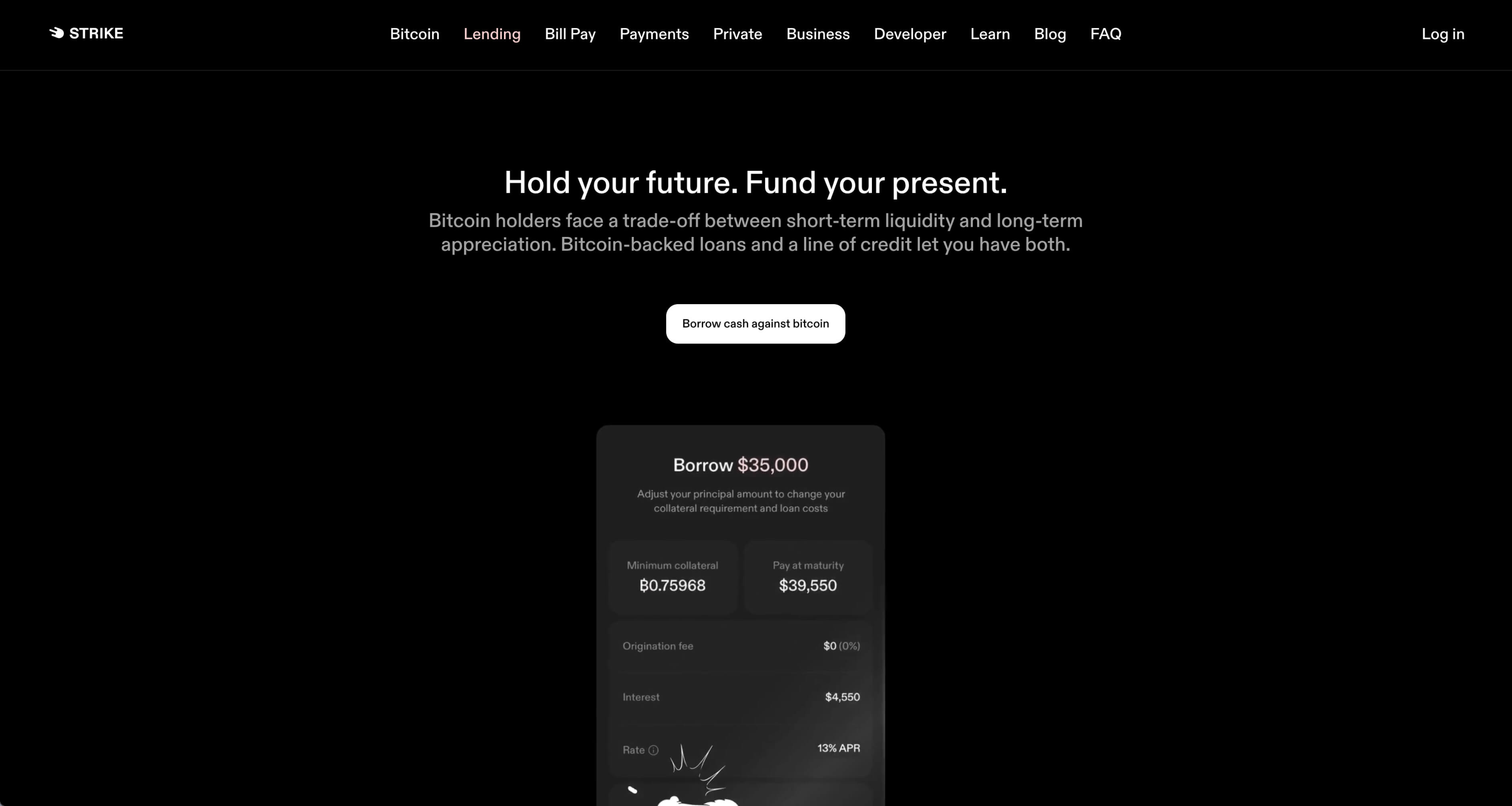

1. Strike: Bitcoin-only fixed-term loans and a revolving line of credit

Strike gives you two ways to borrow against bitcoin: a fixed-term loan and a revolving line of credit. Both products are available to individuals and businesses, so a personal holder and a company treasury can access the same lending infrastructure. Lending services are provided through Zap Solutions Capital, Inc., dba Strike Lending.

Strike's fixed-term loan works like a traditional bitcoin-backed loan. You borrow a lump sum, post bitcoin as collateral, and repay over a 12-month term. The Annual Percentage Rate is fixed for the life of the loan and tiered by loan size. Refinancing is available at maturity or after 60 days in supported states, so borrowers can effectively extend or adjust their loan without needing to pay back principal first.

Strike's line of credit is a revolving facility. You establish a credit line backed by your bitcoin, then draw and repay cash as many times as you want, with no maturity date on principal. Interest accrues daily on only the amount you have drawn, not the full credit line. The Annual Percentage Rate is 13%, calculated as the US Prime Rate (6.75%) plus a 6.25% margin, recalculated quarterly. The line of credit is available to consumers in 38 U.S. states plus D.C. and Puerto Rico, and to businesses in 46 U.S. states plus D.C.

Strike uses a tiered margin system that gives borrowers room to respond when bitcoin's price drops. A margin call triggers at 70% LTV, and you have 72 hours to add collateral or reduce your balance before a partial liquidation occurs. When liquidation does occur, it is partial. Strike sells only enough collateral to bring the LTV back to 65%, which works out to roughly 14% of the collateral at 70% LTV. If LTV reaches 85%, a larger partial liquidation is triggered immediately without the 72-hour grace period, selling approximately 57% of collateral to restore the target LTV. The remaining collateral stays in custody.

Lending services are provided through Zap Solutions Capital, Inc, dba ‘Strike Lending’. Collateral is held by Strike Lending or one of its capital providers in segregated wallets with no further rehypothecation. The bitcoin collateral is never lent out, shorted, or transferred to any other third party.

Repayment supports ACH, wire transfer, and bitcoin, so borrowers can use standard bank transfers rather than being limited to stablecoins or wire-only options. Beyond lending, Strike is a full Bitcoin financial services platform. Borrowers can buy and sell bitcoin, send and receive payments, and manage their holdings, all within the same app where they borrow.

Pros

- No origination, prepayment, late payment, or liquidation fees, so the APR represents the total cost of borrowing

- Flexibility on opening and consolidating multiple active loans, refinancing, and retrieving collateral

- Bitcoin-only collateral means the loan isn't entangled with altcoin volatility, DeFi protocol risk, or multi-chain infrastructure

Cons

- Lending availability and minimums vary by product, borrower type, and state. Fixed-term loans start at $5,000 in some markets, and line-of-credit availability varies by borrower type and state.

- The lowest APRs are reserved for larger loans

- No stablecoin disbursement, only US dollars

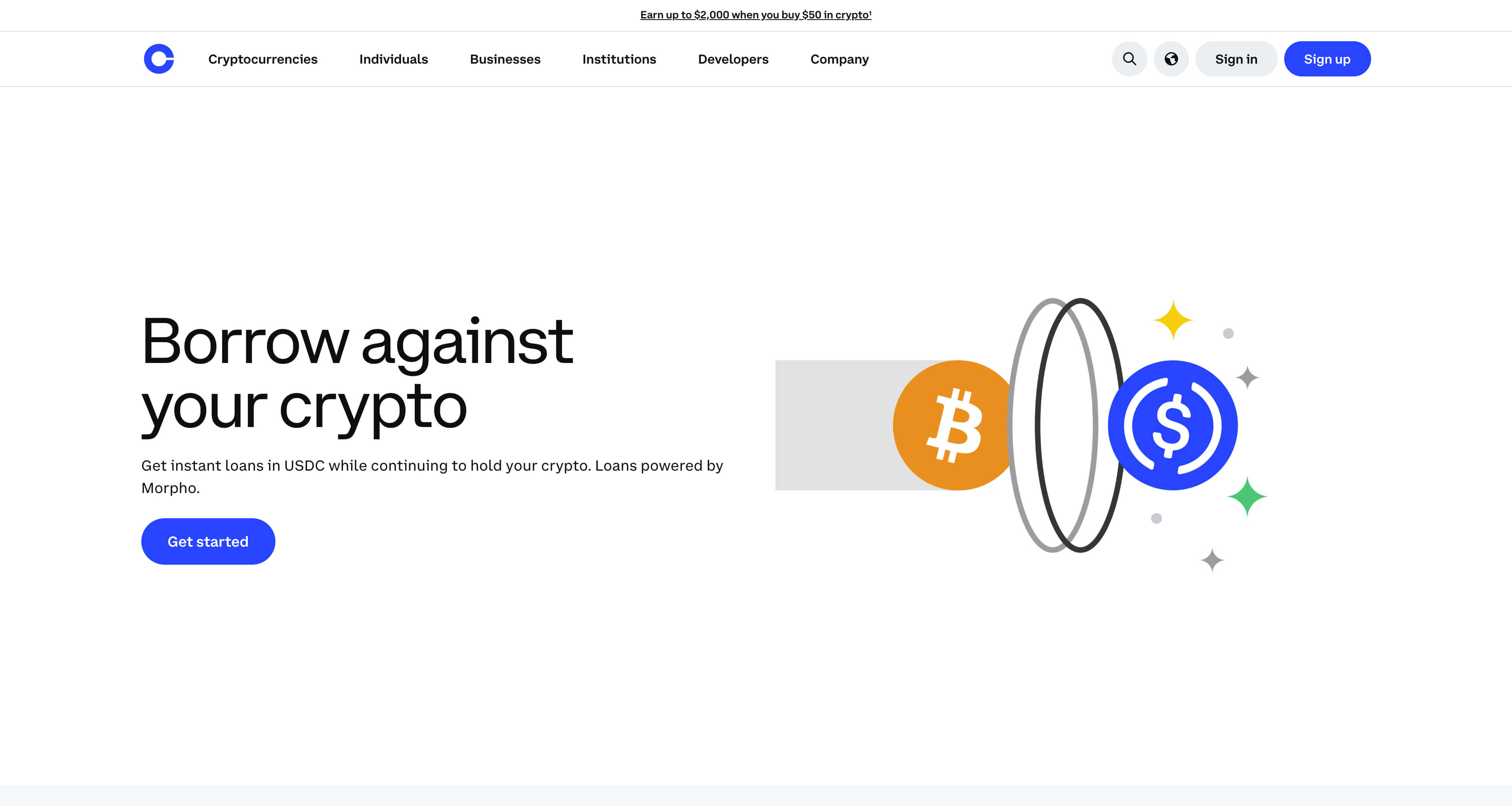

2. Coinbase: Low rates to borrow against cbBTC

Coinbase routes its bitcoin-backed borrowing through Morpho, a decentralized lending protocol running on Base, Coinbase's own Ethereum Layer 2 blockchain. The architecture determines where your bitcoin goes and who controls what happens to it.

When you deposit bitcoin as collateral, Coinbase wraps it into cbBTC, an ERC-20 token on the Base network. Your collateral is actually a derivative token on a different chain, secured by a different consensus mechanism, held inside a smart contract governed by Morpho's protocol logic. The collateral backing your loan is no longer the asset you started with. It is a derivative of that asset, dependent on the bridge infrastructure connecting the two networks and the smart contract code managing the pool.

Coinbase advertises variable rates as low as 5%, but Morpho sets rates algorithmically based on real-time pool utilization. When few borrowers are drawing from the pool, rates stay low. When demand increases, rates rise automatically, with no ceiling and no advance notice. The rate a borrower sees when opening a loan is not a locked rate. It can change hour to hour.

The liquidation mechanism operates through the smart contract itself. Once a borrower's LTV crosses the liquidation threshold, any participant in the Morpho protocol can trigger the liquidation, not just Coinbase. There is no margin call, no grace period, and no opportunity to add collateral before execution. The entire position is liquidated, not just a portion, and a penalty fee is applied to the liquidated amount.

Loan proceeds arrive as USDC, a stablecoin, rather than US dollars in a bank account. Borrowers who need spendable cash face an additional conversion step.

Pros

- No origination fee and no repayment schedule give borrowers full control over the timing and pace of repayment

- Publicly listed company

- Part of a broader ecosystem, so borrowers already on Coinbase can manage lending alongside their existing accounts

Cons

- Collateral is held as cbBTC, not as BTC

- Collateral is locked until full repayment, with no way to retrieve excess bitcoin even if the price rises significantly

- Proceeds arrive as USDC, not USD, requiring an extra conversion step to access cash

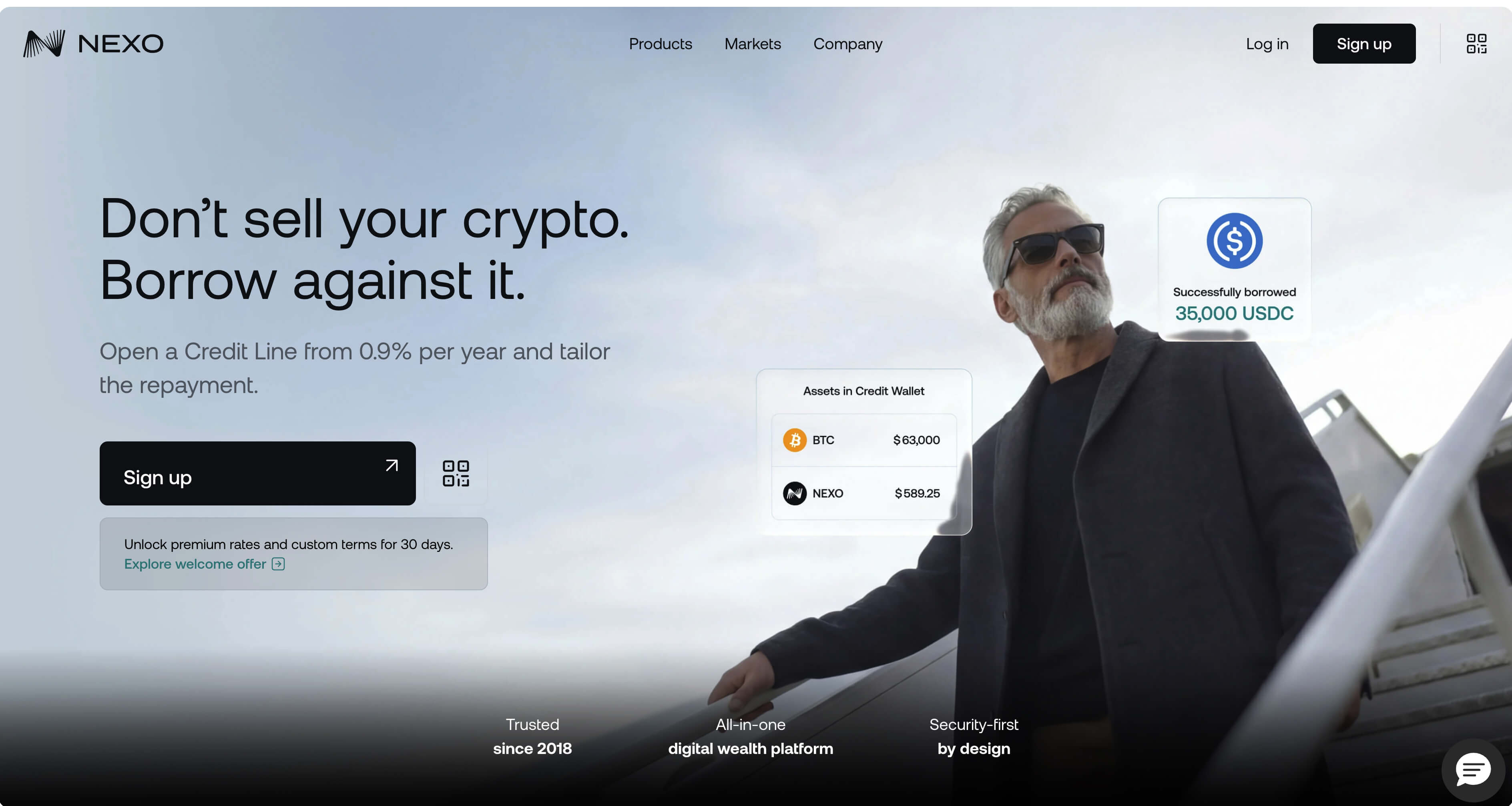

3. Nexo: Low rates for NEXO token holders

Nexo is a multi-asset lending platform that has operated globally since 2018. In 2022, the company reached a $45 million settlement with the SEC and state regulators related to its Earn Interest Product. Nexo returned to the US in February 2026 through a partnership with Bakkt, a US-listed digital asset company providing the regulated trading infrastructure.

Since the relaunch is recent, some details for US borrowers are still being finalized. Nexo's own help center disclaims applicability in the US, and the US-specific rates, terms, and product features have not been publicly detailed. The global product advertises rates as low as 1.9%, but that floor rate is available only to Platinum-tier loyalty members who hold at least 10% of their portfolio in NEXO tokens. Whether this tier system applies to US accounts has not been confirmed.

Nexo accepts over 60 different assets as collateral, including a wide range of altcoins, stablecoins, and tokens, making it one of the most flexible platforms in terms of what you can pledge. Bitcoin is one option among many, and the platform's infrastructure and risk management are designed around this multi-asset model. Nexo's terms permit rehypothecation of collateral, meaning the company can lend, stake, or otherwise deploy your bitcoin for its own purposes while it secures your loan.

Pros

- Low minimum loan size

- No origination fee keeps upfront costs at zero

- No repayment deadlines or minimum installments, so borrowers control the timing of every repayment

Cons

- Whether the NEXO token loyalty tier system applies to US accounts is unconfirmed, meaning the advertised rates may not reflect what US borrowers will actually pay

- The product focuses more on altcoins than on Bitcoin

- The US relaunch is recent (February 2026), limiting availability

4. SALT: The oldest bitcoin-backed lender

SALT has been originating bitcoin-backed loans since 2016, making it one of the longest-running platforms in this category. The company accepts both bitcoin and several altcoins as collateral, and borrowers can structure terms across 1-, 3-, or 5-year durations.

The cost structure layers multiple fees on top of the interest rate. A 1% origination fee is deducted from loan proceeds, so the cash a borrower receives is less than the stated loan amount. If bitcoin's price drops enough to trigger a margin event at 90.91% LTV, what happens next depends on the borrower's setup. Borrowers who have opted in to Stabilization get an intermediate step: SALT automatically converts a portion of collateral to a USD stablecoin to prevent further loss, with a 3% fee on the converted amount. Borrowers who have not opted in to Stabilization skip this step and go directly to full liquidation, with a 5% Liquidation Fee on the collateral sold.

SALT also offers SALT Shield, an optional paid add-on that replaces the standard margin call process entirely with automated downside protection, removing the Stabilization and Liquidation Fees. The protection comes with an upfront fee and restricts collateral withdrawals while active. Borrowers who don't purchase Shield are subject to the standard margin call process and its associated fee schedule.

SALT is a lending-only platform. There is no functionality for buying, selling, or holding bitcoin within the app. Every other aspect of managing a bitcoin position, from accumulating to transacting to custody, requires a separate provider.

Pros

- Lower APRs available for lower LTVs

- Mid-loan collateral retrieval is available, subject to maintaining the loan's LTV requirements

- $5,000 minimum makes it accessible to borrowers with a smaller bitcoin position

Cons

- The 1% origination fee is deducted from the loan proceeds, reducing the cash you receive upfront

- Accessing features like Stabilization and Shield requires separate fees on top of the interest rate and origination fee

- Lending-only platform, so you'll need a separate app for buying, selling, or managing bitcoin

5. Ledn: Tiered pricing on custodied bitcoin loans

Ledn now prices its bitcoin-backed dollar loans by loan size rather than with a single flat rate. On Ledn's public loan calculator as of March 26, 2026, the displayed APR is 10.99% for loans under $250,000, 10.49% at $250,000+, 9.99% at $500,000+, and 9.75% at $1 million+. The new pricing now applies not just to new loans, but also to refinances and renewals. Existing loans keep their current rate until they are renewed or refinanced.

The underlying product remains a 12-month loan issued at a 50% initial LTV, with no prepayment penalties and no monthly payments while the loan is open. For US borrowers, Ledn's help center says the 2% administrative fee charged in some other jurisdictions does not apply. The company is now explicit that its dollar loans are structured as custodied loans: bitcoin collateral stays in custody, may only be re-posted to a trusted USD funding partner to secure financing, and neither Ledn nor the funding partner can lend it out to generate interest.

The collateral retrieval policy is still restrictive. To withdraw excess collateral, a borrower's LTV must fall below 30%, the loan must be at least 60 days old, and withdrawals are capped at $100,000 per rolling 60-day period. After each retrieval, the LTV rebalances to 40%. In practice, even a significant rise in bitcoin's price unlocks only a narrow window for partial withdrawal, with a cooling period before the next one.

Ledn remains more lender than platform. It offers useful loan-management features such as top-ups, partial repayments, and proof-of-reserves/Open Book reporting, but it still lacks the payments, wallet, and broader app ecosystem that distinguish full-service Bitcoin financial platforms from lending specialists.

Pros

- Bitcoin-only collateral with a custodied-loan structure where collateral is not lent out to earn interest

- $500 minimum keeps the product accessible to smaller borrowers, while larger loans now unlock lower advertised APRs

- No monthly payments or prepayment penalties, with repayment options that include BTC collateral, USDC, ACH, and wire transfer

Cons

- The best pricing is reserved for large loans, so smaller borrowers get the top tier

- Not available in approximately 10 states, including California and Connecticut

- Limited platform beyond lending and trading, with no payment wallet or broader Bitcoin financial services

6. Figure: HELOC lender offering crypto-backed loans

Figure is a fintech company that has originated more than $9 billion in loans, primarily home equity lines of credit, personal loans, and mortgage refinances, built on its Provenance blockchain. Bitcoin-backed lending is a newer and smaller part of the business. The company holds state lending licenses and a BBB A+ rating, both established through its traditional lending operations.

Figure's bitcoin-backed loan accepts bitcoin and several altcoins as collateral, and offers an initial LTV of up to 75%. A higher initial LTV means borrowers can post less collateral per dollar borrowed, but it also narrows the buffer between the starting position and a liquidation event.

Figure offers Liquidation Protection as an optional paid add-on in select states, but has not publicly detailed the cost or terms. Without it, a 2% liquidation fee applies to any collateral sold during a margin event, in addition to the 1% origination fee deducted from the initial disbursement.

Rates on Figure's bitcoin-backed loans "change frequently," per the company's own disclosure. The APR a borrower sees at the time of application may differ from the rate listed on the website earlier that week. There is no published rate lock mechanism.

Collateral is held in a segregated MPC wallet with a verifiable on-chain address, and Figure states it does not rehypothecate. Once deposited, however, collateral cannot be retrieved until the loan is repaid in full, regardless of how much bitcoin's price appreciates during the term. Figure is a lending-only platform with no bitcoin buying, selling, or payment functionality.

Pros

- Interest deferral to maturity eliminates monthly payment obligations, letting borrowers settle everything at the end of the term

- Collateral held in a segregated MPC wallet with a verifiable on-chain address. Borrowers can confirm custody at any time, and Figure states it does not rehypothecate

- Offers HELOC and other types of loans

Cons

- The 1% origination fee and 2% liquidation fee stack, so if you're liquidated, you pay both

- Rates "change frequently" per Figure's own disclosure, so the APR at time of application may differ from what is advertised

- No way to retrieve excess collateral while the loan is active, even if bitcoin's price rises substantially. Everything is locked until full repayment

7. Unchained: $150K+ loans for businesses

Unchained's lending product is built on a 2-of-3 multisig custody model. The borrower holds one key, Unchained holds one, and an independent third party holds the third. No single entity can unilaterally move the collateral, and the bitcoin is verifiable on-chain at any point during the loan.

The multisig structure creates trade-offs in both liquidation and cost. Selling a portion of collateral in a multisig vault requires a coordinated on-chain transaction among key holders. Partial liquidations are operationally impractical in this setup. When a margin call results in forced selling, the entire collateral position is liquidated. Coordinating multiple key holders for every collateral movement adds complexity that shows up in the interest rate: 14.18% APR, with no published tiers for larger loans to bring it down. That higher cost and full-liquidation risk is the trade-off for a custody model where no single entity controls the bitcoin.

Unchained's lending product is only available to business entities. Individuals, sole proprietors, and personal bitcoin holders cannot borrow. The minimum loan is $150,000, and a 2% origination fee means at least $3,000 in upfront costs before any interest accrues.

Beyond lending, Unchained offers collaborative custody vaults, IRA accounts, and inheritance planning, all anchored to the same multisig infrastructure.

Pros

- US-based and state-licensed, with coverage across 42 states

- Bitcoin-only: no altcoin infrastructure, no multi-chain complexity

- Collaborative custody, IRA, and inheritance planning are available alongside lending, creating a broader Bitcoin financial services relationship

Cons

- Only available to business entities. Individuals and sole proprietors cannot borrow

- The 2% origination fee on a minimum $150,000 loan means at least $3,000 upfront before interest

- 14.18% APR with no published volume-based tiers to bring it down

8. Arch: Borrow against BTC, ETH, and SOL

Arch positions its product closer to a credit facility than to a traditional fixed-term loan. The 12-month term serves as a framework for borrowers to upsize their loan as bitcoin's price appreciates, add collateral to access more liquidity, withdraw excess collateral when LTV permits, and repay at any time. Refinancing is available at maturity, so the relationship can extend beyond the initial term.

Arch accepts both bitcoin and several altcoins as collateral, with its infrastructure built to support multiple asset types across the collateral pool. Rates are tiered by loan size, with larger loans receiving lower APRs. Each borrower's collateral is held in a segregated, on-chain, verifiable cold-storage address, and Arch provides a 20-day grace period for late interest payments before any enforcement action.

The fee structure includes a 1.49% origination fee deducted from loan proceeds and a 2% fee on any collateral liquidated during a margin event.

Arch is a lending-only platform with no functionality for buying, selling, or managing bitcoin. Borrowers who want to accumulate, transact, or otherwise manage their holdings need a separate provider.

Pros

- Each borrower's collateral is in a segregated cold-storage address, verifiable on-chain at any time

- 20-day grace period for late interest payments before any enforcement action

- $1,000 minimum makes it accessible to smaller borrowers

Cons

- 1.49% origination fee reduces the loan proceeds you receive

- A 2% fee on the liquidated amount adds cost during an already painful price decline

- Lending-only platform with no way to buy, sell, or manage bitcoin within Arch

Questions to consider when choosing a bitcoin-backed lender

Should I just pick the lender with the lowest advertised rate?

Not necessarily. Some platforms advertise an interest rate rather than an APR, so costs like origination fees aren't reflected in the headline number. The advertised rates you see sometimes come with conditions, such as minimum loan sizes or maximum LTVs, that limit how much you can actually borrow at that price. Liquidation fees, processing fees, and early-repayment penalties vary across lenders and aren't reflected in the APR.

What's the trade-off between bitcoin-only and multi-asset collateral?

Bitcoin-only lenders don't manage altcoin volatility, multi-chain infrastructure, or DeFi protocol integrations, which can simplify custody and reduce the categories of risk your collateral is exposed to. A narrower focus can also give the team more bandwidth to improve the core product, reduce costs, and expand into complementary services. Multi-asset platforms offer more flexibility in what you can pledge, but that flexibility can introduce operational complexity in how your bitcoin is held and how liquidations are executed.

What's the difference between a fixed-term loan and a revolving line of credit for borrowing against bitcoin?

A fixed-term loan provides a lump sum with a defined repayment schedule, maturity date, and fixed rate. That makes it a better fit for larger, planned expenses where you know the amount upfront. A revolving line of credit allows repeated draw-and-repay activity against the same collateral, with interest accruing only on the outstanding draw, making it more useful for ongoing, day-to-day spending the way you might use a credit card. Revolving rates are typically variable, and the open-ended structure means LTV requires ongoing attention as the drawn balance and bitcoin's price fluctuate.

How do margin call and liquidation policies differ across lenders?

Four variables differ: the buffer between the maximum starting LTV and the liquidation threshold, the amount of notice given before forced selling begins, whether the lender sells just enough collateral to restore a target LTV or the entire position at once, and the fee charged on the amount liquidated. A wider LTV buffer means bitcoin's price has to fall further before a margin call is triggered. A grace period and partial liquidation limit the impact of a price drop. No grace period and full liquidation amplify it.

Does it matter whether a lender is US-based or US-licensed?

It can. US-based, state-licensed lenders operate under domestic regulatory oversight, which generally means clearer legal recourse and consumer protections. Offshore lenders may operate under different regulatory frameworks.

How to choose the best bitcoin-backed lender

The decision comes down to five things:

- Flexibility: Strike is the only platform here that offers both a fixed-term loan and a revolving line of credit. A few others offer revolving credit with no maturity date on principal, and one offers fixed terms of up to five years.

- Cost: APR is the most consistent basis for comparison, but not all fees are reflected in it.

- Custody: These platforms span the full spectrum, from traditional third-party custodians to segregated cold storage with on-chain verification to multisig vaults where the borrower holds a key. Whether a platform accepts only bitcoin or also altcoins and wrapped tokens affects what infrastructure your collateral runs on.

- Availability: Not every lender operates in every US state. Some haven't publicly confirmed their US terms, which means advertised rates may not apply to US borrowers.

- Ecosystem: Some platforms offer broader bitcoin financial services, including buying, selling, and payments, as well as lending. Others are lending-only, so everything outside the loan requires a separate provider.

Every platform on this list solves the same core problem: you need cash, and you don't want to sell your bitcoin to get liquidity. The right lender depends on what you're optimizing for. Pick the one that fits and read the fine print.

Strike is a financial technology company, not a bank. Depending on the region, credit is issued by Zap Solutions Capital, Inc., dba Strike Lending, or Column N.A., Member FDIC. Credit approval and terms are subject to eligibility and collateral requirements. Images are illustrative examples. Loan purposes, terms, and outcomes vary. Bitcoin is volatile, and declines in its price may trigger margin calls and liquidations when used as collateral. Strike and Strike Lending do not offer investment, financial, tax, legal, or professional advice. Consult with financial and tax advisors to understand the risks of buying, selling, holding, and borrowing against your bitcoin.

This article is for informational purposes only. It is not financial advice and does not endorse or recommend any product or service mentioned. Platform data is sourced from each company's publicly available website, help center, regulatory filings, and public marketing materials as of May 11, 2026. Features, fees, rates, and availability are subject to change. Verify any claims independently before making financial decisions.

Borrowing against bitcoin involves risk. If bitcoin's price declines, you may need to post additional collateral, or your collateral may be liquidated to cover the balance. Liquidations may result in a taxable event. Consult a qualified tax professional about the tax implications of borrowing against bitcoin.