Summary: New York's BitLicense sets one of the highest regulatory bars in the US, and roughly 36 entities are licensed to offer bitcoin services in the state. As of 2026, the major options for New York residents include Strike, Cash App, Coinbase, Gemini, Robinhood, PayPal, and bitcoin ATMs. Strike is the only platform among them where bitcoin is the sole focus, offering financial services beyond trading, including bitcoin-backed loans, bill pay from bitcoin, automatic paycheck-to-bitcoin conversion, and fee-free recurring buys. Coinbase, Gemini, and Robinhood operate as multi-asset platforms that also list hundreds of altcoins and offer prediction markets. PayPal and Cash App offer bitcoin buying inside broader payments apps. Bitcoin ATMs provide cash-based purchasing at much higher fees than online platforms.

New York sets the highest bar in the US for platforms that allow customers to buy, sell, or hold bitcoin. The BitLicense, introduced by the New York Department of Financial Services in 2015, requires any company offering virtual currency services to obtain a state license.

The license dictates how a platform handles your money and your bitcoin:

- Segregated custody. Customer funds must be held separately from the company's own assets and safeguarded for the benefit of customers. If the company faces financial trouble, your bitcoin isn't commingled with its balance sheet.

- Capital requirements. Licensees maintain a minimum level of capital set by NYDFS, a financial buffer that reduces insolvency risk.

- AML/KYC compliance. Every licensee runs a Bank Secrecy Act program with transaction monitoring, suspicious activity reporting, and customer identification. NYDFS enforces this independently at the state level, on top of federal requirements.

- Cybersecurity standards. Licensees must maintain a cybersecurity program under 23 NYCRR Part 500, one of the strictest US cybersecurity regimes for financial institutions.

- Regular examinations. NYDFS conducts periodic audits of licensed entities, reviewing books, records, and operations directly.

About 36 entities have been approved to operate in New York, roughly two-thirds holding a BitLicense and the rest operating under a limited-purpose trust charter. Both paths authorize virtual currency business activity under NYDFS oversight.

Every licensed platform offering bitcoin services in New York clears the same regulatory bar. Where they diverge is what happens after you buy. Converting a paycheck to bitcoin, paying bills without selling, and withdrawing to your own wallet are part of living on a bitcoin standard. Not every platform covers the same ground.

| Feature | Strike | Cash App | Coinbase | Gemini | Robinhood | PayPal | Bitcoin ATMs |

|---|---|---|---|---|---|---|---|

| Bitcoin-focused | Yes | Yes | No | No | No | No | Varies |

| Trading fees | 0%–0.89%1 | 0%–2%2 | Dynamic3 | ~1.49%+4 | Spread5 | 1.50%–2.20%6 | 6.5–25%+ |

| Fee-free recurring buys | Yes | Yes | No | No | No | No | No |

| Direct deposit to bitcoin | Yes | Yes | No | No | No | No | No |

| Bill pay from bitcoin | Yes | No | No | No | No | No | No |

| Free on-chain withdrawals | Yes7 | Yes7 | No9 | No9 | No9 | No10 | No |

| Prediction markets | No | No | Yes | Yes | Yes | No | No |

| Business accounts | Yes | No8 | Yes | Yes | No | Yes | No |

| Bitcoin-backed lending | Yes | No | No11 | No | No | No | No |

1 Strike charges no fees on recurring buys. Direct deposit allocations are also fee-free up to $20K/mo. One-time buys start at 0.89% and drop to 0.25% for customers on higher trading tiers.

2 Cash App charges no fees on Auto-Invest or purchases over $2,000. Below $2,000, Cash App charges fees ranging from roughly 0.9% to 2.0%, depending on purchase amount.

3 Coinbase charges dynamic pricing based on payment method, order size, and market conditions, plus a spread. Coinbase Advanced operates on a maker/taker model based on 30-day volume.

4 Gemini charges approximately 1.49% plus a spread per transaction via the app. Through the ActiveTrader interface, they charge 0.20% maker / 0.40% taker at the lowest volume tier, decreasing with volume.

5 Robinhood charges no commission but embeds a spread in the execution price. The exact markup is not publicly disclosed.

6 PayPal charges 1.50% over $1,000. 1.80% $200–$1,000. 2.00% $75–$200. 2.20% under $75. Spread included in quoted price on top of posted fee.

7 Strike and Cash App cover the on-chain network fee on behalf of customers for withdrawals processed in up to 24 hours.

8 Cash App for Business exists as a merchant payments product but does not support bitcoin buying.

9 Coinbase, Gemini, and Robinhood pass on-chain network fees through to the customer on bitcoin withdrawals.

10 PayPal charges 1% of the USD value of bitcoin transferred out, plus a network fee.

11 Coinbase offers crypto-backed loans in other US states but explicitly excludes New York.

1. Strike: Bitcoin-only financial platform

Strike is the only app available in New York focused exclusively on Bitcoin. No altcoins, no stocks. Every feature is built around buying, holding, saving, and spending bitcoin.

Buying bitcoin on Strike starts at a 0.89% fee that drops with monthly volume. Purchases, sales, recurring buys, bill payments, and direct deposit conversions all count toward the next tier, scaling down to 0.25% at the highest volumes.

Recurring buys run on frequencies from hourly to monthly, with no minimum purchase amount. Fees are waived after the first week, making DCA effectively free.

Direct deposit converts your paycheck to bitcoin automatically. You allocate anywhere from 0% to 100% of each paycheck, and the first $20,000 per month in conversions is fee-free. Early direct deposits allow select customers with supported payroll providers to receive their paycheck up to 2 days before the typical payday.

Bill pay lets you pay credit cards, utilities, phone bills, and other recurring expenses from your cash or bitcoin balance. If you pay from bitcoin, Strike handles the conversion and sends the payment. The per-bill limit is $95,000.

Bitcoin-backed loans and a line of credit are available in New York. Fixed-term loans with a 12-month maturity have tiered APRs that start at 9.5% and vary by loan size. The minimum loan amount is $10,000 for consumers and $5,000 for businesses. The revolving line of credit has a variable APR and a minimum of $5,000 for both account types. No credit checks required and zero origination.

Bitcoin withdrawals are free. On the flexible withdrawal option, Strike covers the on-chain network fee on behalf of the customer, with settlement within 24 hours. Auto-withdrawals move your bitcoin to your own wallet once your balance crosses a threshold you set, with a minimum of 0.01 BTC.

Lightning Network is built natively into the platform. Strike's founder, Jack Mallers, was an early Lightning pioneer. His first product, Zap, was one of the first Lightning wallets in 2018, built on the idea that Bitcoin could scale through a second layer for everyday transactions rather than increasing the block size and risking a chain split. Strike runs its own Lightning infrastructure end to end, and every account gets a Lightning address for convenient instant payments.

Strike Private provides dedicated support, custom pricing, and deep liquidity for bitcoin orders above $1 million.

Business accounts are available for companies that want to buy, hold, or use bitcoin as part of their operations.

Pros:

- Bitcoin is Strike's only priority

- Direct deposit converts up to 100% of each paycheck to bitcoin, fee-free up to $20K/month

- Bill pay, bitcoin-backed loans and line of credit, free bitcoin withdrawals with on-chain fees covered, and native Lightning go beyond buying and selling

- Recurring buy fees are waived after the first week, incentivizing regular saving habits

Cons:

- One-time buy fees start at 0.89% before volume discounts

- Debit card purchases carry higher fees than ACH-funded buys

- No order book or maker/taker fee structure for exchange-style trading

- Fee-free direct deposit conversion capped at $20,000 per month. Standard fees apply above that

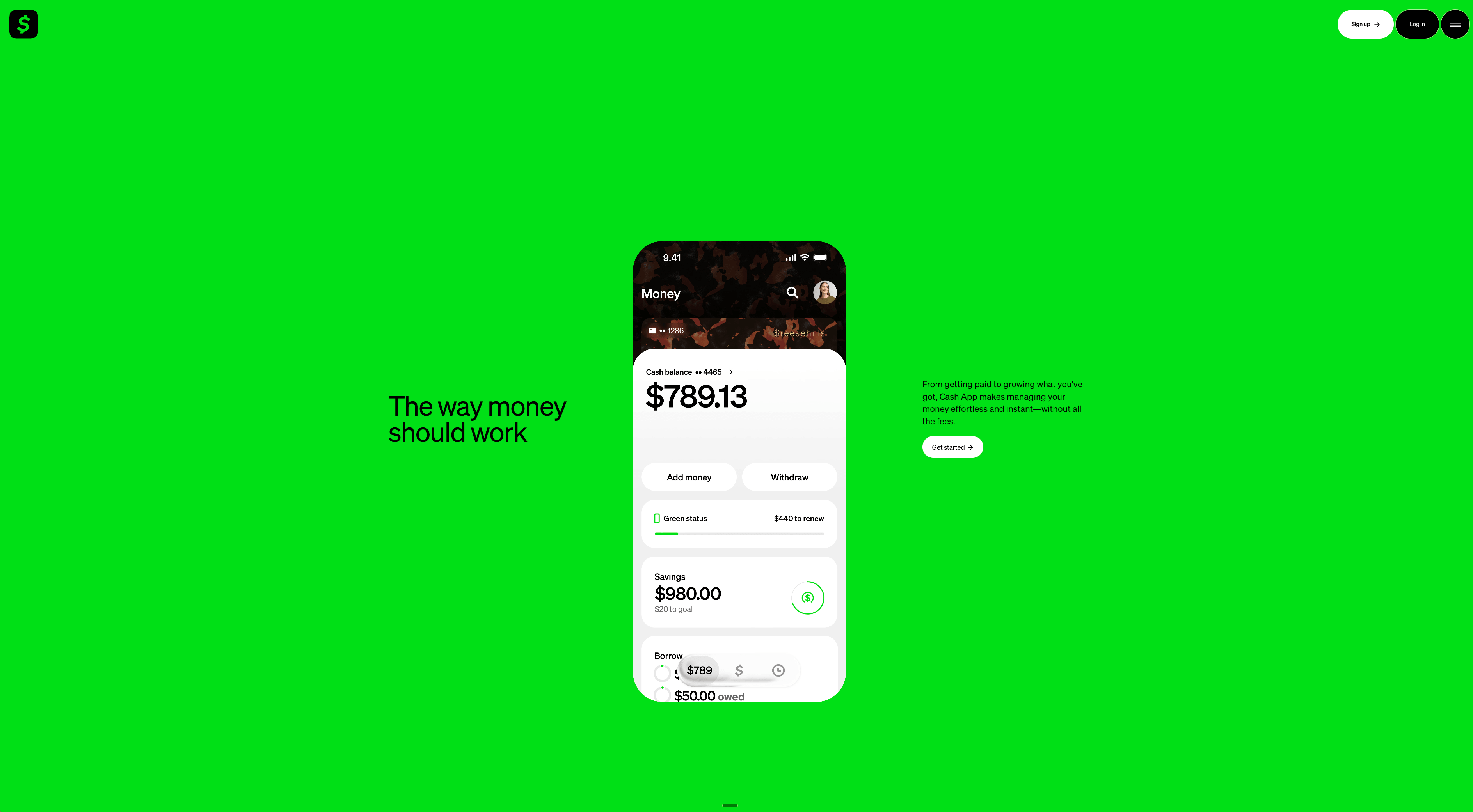

2. Cash App: Bitcoin buying inside a payments app

Cash App started as a payments app from Square, now Block Inc., and added bitcoin buying in 2018. Bitcoin has since become a bigger part of the product, but Cash App remains a general financial app where customers also buy and sell stocks.

Cash App does not offer altcoins. For bitcoiners, that's a meaningful distinction, even though bitcoin is one feature inside a broader product rather than the app's central focus.

As of 2026, Cash App charges no fees on manual bitcoin purchases over $2,000. For purchases under $2,000, Cash App reduced its fees, with rates ranging from roughly 0.9% to 2.0% depending on the purchase amount. Automatic purchases through Auto-Invest, Paid in Bitcoin, and Round Ups are fee-free regardless of size.

Cash App supports on-chain bitcoin withdrawals to external wallets and Lightning Network payments in most US states, but Lightning is not available in New York.

Direct deposit is available, and customers can set up automatic recurring bitcoin purchases. Cash App does not offer bill pay from bitcoin.

Pros:

- No altcoins. Bitcoin-only

- Fee-free and spread-free bitcoin purchases over $2,000 as of February 2026

- Supports bitcoin withdrawals to external wallets, with bitcoin held 1:1

- Focuses on features that encourage saving habits, like round-ups

Cons:

- Bitcoin is a feature inside a payments and investing app, not the core product. Stock trading and other financial services share the product roadmap

- Fees of 0.9%–2.0% on manual purchases under $2,000, making small buys expensive outside Auto-Invest

- Lightning Network not available in New York

- No bill pay from bitcoin or advanced trading features like limit orders

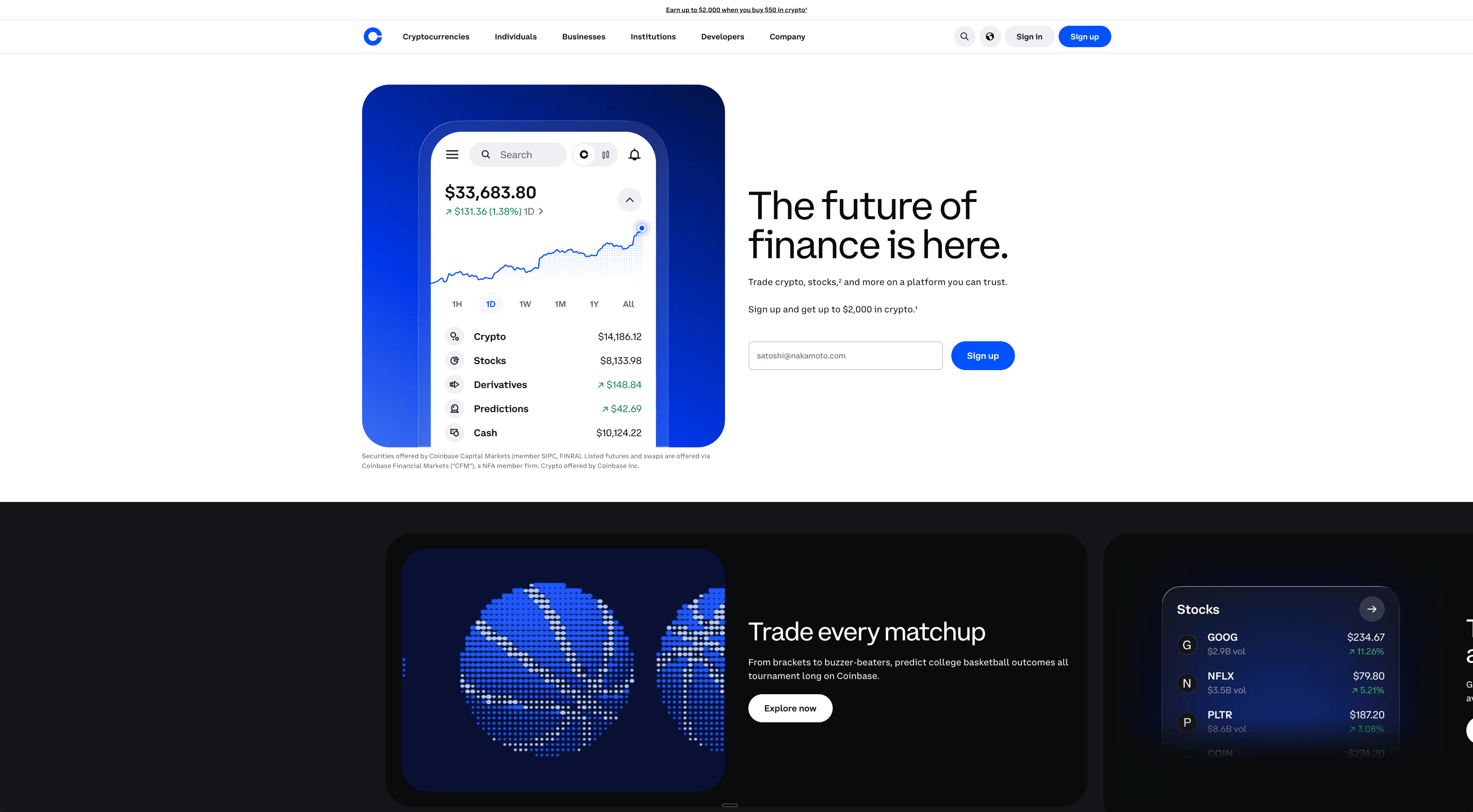

3. Coinbase: Largest US cryptocurrency exchange

Coinbase is the largest exchange in the United States, with over 100 million customers globally, including businesses and institutions. It lists bitcoin alongside more than 250 altcoins and has expanded into derivatives and futures through its CFTC-regulated derivatives exchange. Bitcoin is one asset in a trading-oriented marketplace built around breadth.

In 2017, during the Bitcoin block size wars, Coinbase signed the New York Agreement backing SegWit2x, a proposed hard fork that would have doubled Bitcoin's block size. The debate split the community between those who wanted to scale through larger blocks and those who favored second-layer solutions like the Lightning Network. SegWit2x was abandoned after failing to reach consensus.

The Coinbase Wallet, a self-custodial standalone app launched in 2018 and renamed to Base App in 2025, still does not support Bitcoin.

Coinbase charges on-chain network fees for bitcoin withdrawals to external wallets, reducing the amount that reaches your wallet. Coinbase added Lightning Network support in 2024 through an integration with Lightspark, a third-party infrastructure provider.

Coinbase's standard app uses dynamic pricing based on payment method, order size, and market conditions, with a spread included in the quoted price. The app does not display a fixed fee schedule, making it difficult to know the exact cost before placing an order. Coinbase Advanced uses a maker/taker model based on 30-day trading volume, with lower rates than the standard app.

Coinbase does not offer fee-free recurring buys, direct deposit to bitcoin, or bill pay from bitcoin.

In January 2026, Coinbase launched prediction markets in partnership with Kalshi, a CFTC-regulated exchange. Customers can wager on outcomes in sports, politics, economics, and entertainment.

Pros:

- Largest US exchange with deep liquidity and a track record since 2012

- Coinbase Advanced offers competitive maker/taker fees for high-volume traders

- Publicly traded on NASDAQ since 2021, with financial transparency through quarterly SEC filings

- Offers credit card with bitcoin rewards

Cons:

- Standard app uses dynamic pricing with no fixed fee schedule, making costs unpredictable. Advanced tier fees require a separate interface

- Lists bitcoin alongside 250+ altcoins, derivatives, and futures in a trading-oriented marketplace

- Prediction markets for sports, politics, and entertainment launched January 2026, drawing focus away from bitcoin

- Bitcoin withdrawals incur network fees, reducing the amount that reaches your wallet

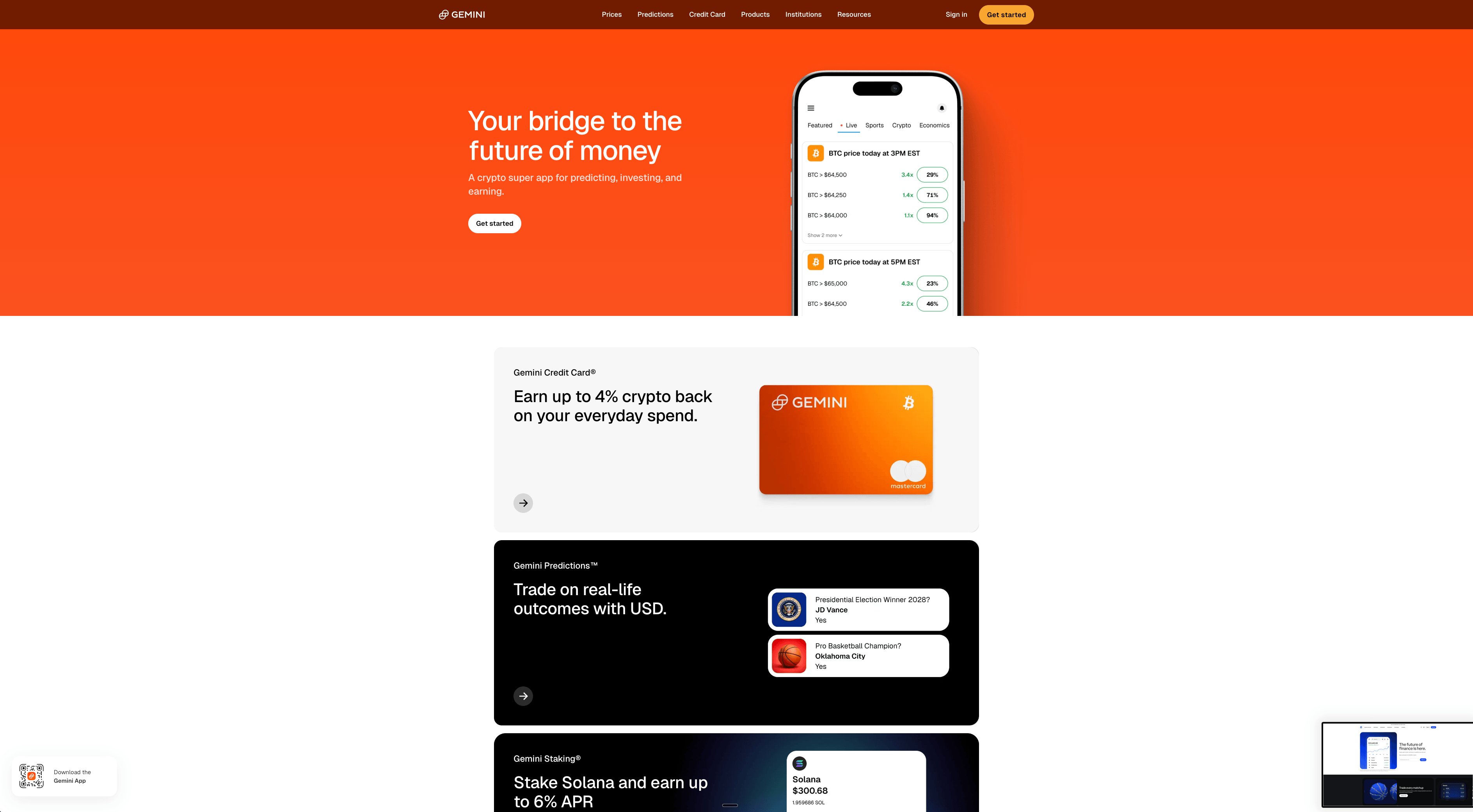

4. Gemini: NYC-headquartered cryptocurrency exchange

Gemini is a trading platform founded in New York City by Cameron and Tyler Winklevoss. It was among the first companies to receive a BitLicense, and serves both retail and institutional clients with dedicated business accounts.

The standard Gemini app charges a convenience fee of approximately 1.49% plus a spread on each transaction. That's the default fee most customers encounter.

Gemini's ActiveTrader interface offers lower rates through a volume-based maker/taker schedule: 0.20% maker and 0.40% taker at the lowest tier, decreasing to 0.10% maker / 0.25% taker at $50,000 in monthly volume. Above $50M, maker fees drop to 0% and taker fees to 0.05%. Accessing these rates requires switching to the ActiveTrader interface.

The platform lists bitcoin alongside over 100 altcoins and offers staking and a credit card with bitcoin rewards.

Gemini previously operated Gemini Earn, a program where customers lent their assets to Genesis Global Capital. In November 2022, Genesis froze withdrawals, affecting over 232,000 Gemini Earn customers. Genesis filed for bankruptcy in January 2023. Gemini contributed $50 million toward recovery and settled with the New York Attorney General over the matter.

Customers ultimately received 100% of their assets in kind by June 2024, when the recovered assets were worth 237% of their value at the time of the freeze. The program is now permanently discontinued.

Gemini charges on-chain network fees for bitcoin withdrawals. Gemini does not offer direct deposit conversion to bitcoin, bill pay from bitcoin, or Lightning Network support.

In December 2025, Gemini launched Gemini Predictions, offering event contracts on sports, politics, and economics across all 50 states. Customers can wager on NFL and college football games, complete with team logos.

Pros:

- ActiveTrader fees start at 0.20% maker / 0.40% taker and decrease with volume

- Founded and headquartered in New York with a strong compliance record

- Credit card with bitcoin rewards on everyday spending

- Supports multiple fiat deposit methods including ACH and wire transfer

Cons:

- Standard app charges approximately 1.49% plus a spread per transaction. ActiveTrader's lower rates require navigating to a separate interface

- Lists 100+ altcoins alongside bitcoin

- Gemini Earn resulted in 232,000+ customers having funds frozen through the Genesis bankruptcy

- Prediction markets for sports, politics, and economics launched in December 2025, moving them further away from a bitcoin focus

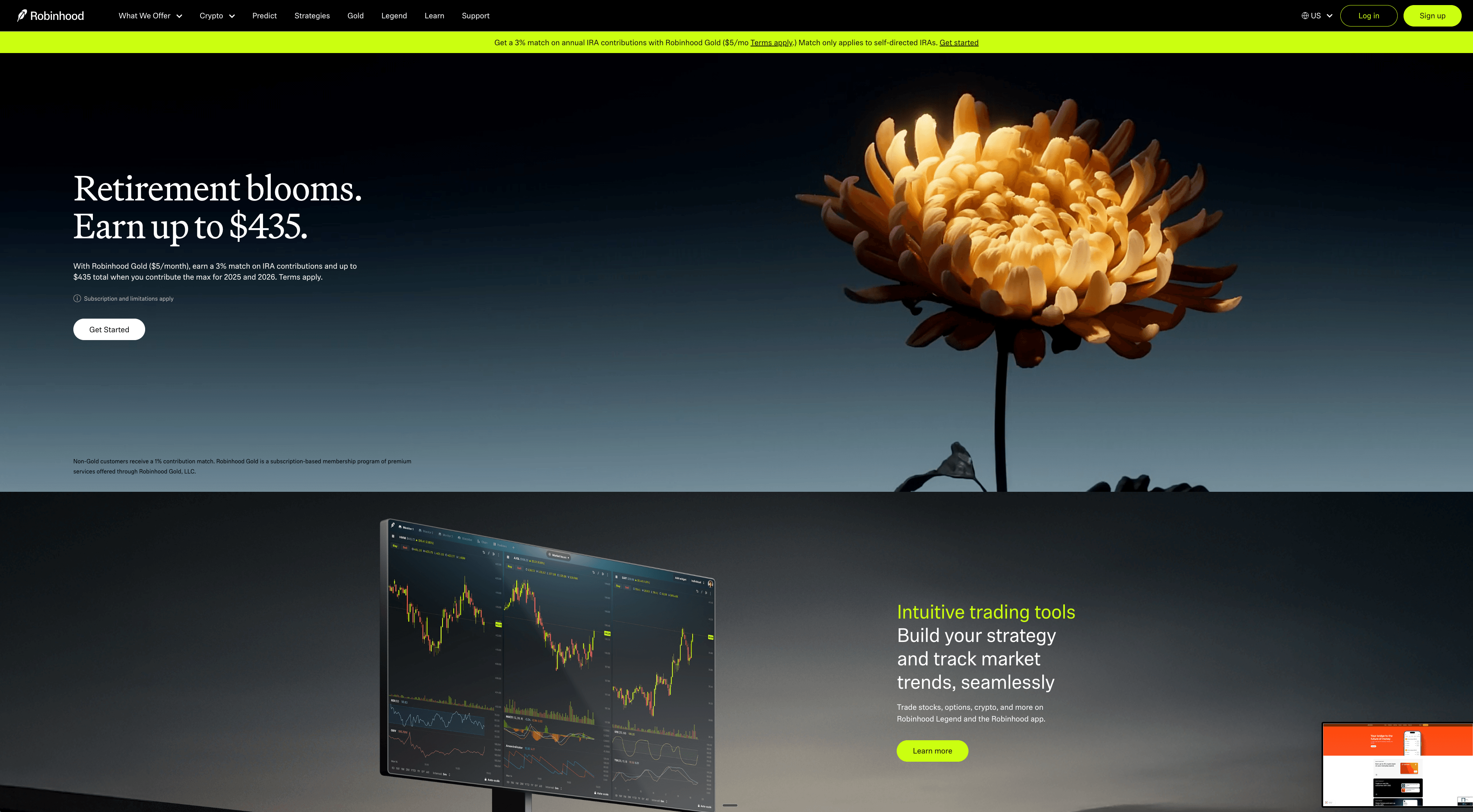

5. Robinhood: Multi-asset brokerage

Robinhood is a multi-asset brokerage offering stocks, options, ETFs, and bitcoin alongside over 20 altcoins through a single app. In June 2025, Robinhood completed its $200 million acquisition of Bitstamp, one of the longest-running exchanges, adding exchange-grade infrastructure and deeper liquidity.

Robinhood charges 0% commission on trades but embeds a spread in the execution price. The exact spread percentage is not publicly disclosed. The cost of each trade is not displayed as a line-item fee, making it harder to know exactly what you're paying on any given purchase.

Robinhood supports bitcoin withdrawals to external wallets, but the feature didn't arrive until 2022, four years after the platform first listed bitcoin for trading in 2018. For those four years, customers could buy and sell bitcoin on Robinhood but couldn't move it to their own wallet. Robinhood does not charge a withdrawal fee, but on-chain network fees are passed through to the customer. The platform does not support Lightning Network, bill pay from bitcoin, or direct deposit conversion to bitcoin. Robinhood does not offer business accounts.

Prediction markets have become one of Robinhood's fastest-growing product areas. Robinhood offers event contracts on sports, politics, economics, and culture. When a platform's momentum is in event-based wagering, the features that get attention next are more likely to serve that growth than to deepen bitcoin-specific tools.

Pros:

- Easy-to-use interface

- Supports bitcoin withdrawals with no Robinhood fee, though network fees apply

- Bitstamp acquisition adds institutional-grade exchange infrastructure

- Bitcoin, stocks, ETFs, and options accessible from a single account

Cons:

- Undisclosed spread is embedded in the price, making true costs less transparent than a posted fee

- Bitcoin is a secondary feature within a multi-asset brokerage built around stocks and options

- Prediction markets are among the platform's fastest-growing product areas, diverting focus away from bitcoin

- No Lightning Network, bill pay, or direct deposit to bitcoin

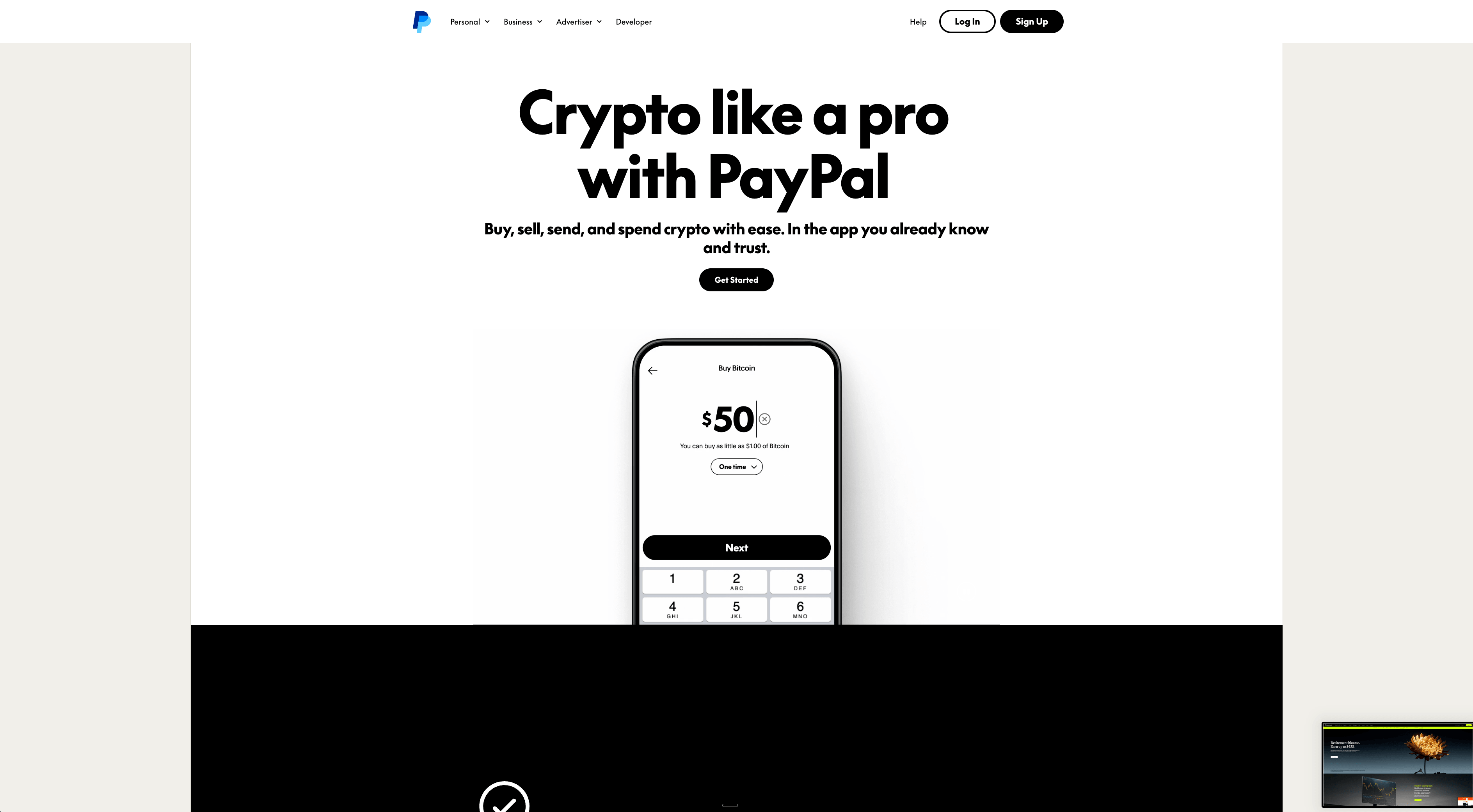

6. PayPal: Bitcoin buying inside a payments giant

PayPal added bitcoin buying and selling in 2020. Bitcoin is a feature within an app built for online payments, peer-to-peer transfers, and checkout services. PayPal's sister app, Venmo, also offers bitcoin buying with a similar fee structure, extending bitcoin access across both platforms. Eligible business accounts on PayPal can also buy and sell bitcoin.

PayPal charges a tiered fee on every bitcoin purchase: 2.20% on transactions under $75, scaling down to 1.50% over $1,000. A spread is included in the quoted exchange rate on top of the posted fee, making the total cost higher than the fee alone suggests.

Bitcoin trading on PayPal and Venmo is operated through Paxos Trust Company. PayPal now supports external wallet transfers for bitcoin, but the feature wasn't available at launch. For nearly two years, customers could buy and sell bitcoin inside the app but couldn't withdraw it to an external wallet. External transfers launched in June 2022, with a 1% fee on the USD value of bitcoin transferred out plus a network fee. Transfers between PayPal and Venmo accounts are free.

PayPal has leaned heavily into its stablecoin, PYUSD, offering approximately 4% rewards for holding it. Neither PayPal nor Venmo offers direct deposit to bitcoin, bill pay from bitcoin, Lightning Network support, or fee-free recurring buys.

Pros:

- Familiar interface for the hundreds of millions of existing PayPal customers

- External bitcoin wallet transfers now supported

- Free bitcoin transfers between PayPal and Venmo accounts

- Business accounts can buy, sell, and hold bitcoin alongside PayPal's standard commerce tools

Cons:

- Fees of 1.50%–2.20% plus an undisclosed spread make it one of the more expensive online options

- Bitcoin trading is operated through Paxos, a third-party custodian, not PayPal directly

- No direct deposit to bitcoin, bill pay, Lightning Network, or fee-free recurring buys

- Platform focus is on payments and stablecoin products, not bitcoin-specific tools

7. Bitcoin ATMs: Cash-based buying at retail locations

Bitcoin ATMs are physical kiosks that allow you to buy bitcoin with cash. Bitcoin ATM operators in New York must hold a BitLicense, which limits the field. Several of the largest national chains don't hold a BitLicense and don't operate in the state.

Bitcoin ATMs charge the highest fees of any buying method. Posted fees typically range from 6.5% to 20%, but the total cost including exchange rate markups often reaches 10% to 25% or more. Some operators set exchange rates significantly below market price, effectively adding a hidden markup on top of posted fees.

A $1,000 purchase at a bitcoin ATM could cost $100 to $250 in fees, compared to under $15 on the online platforms listed above at their standard rates. That difference is bitcoin that never reaches your wallet.

KYC requirements apply to all transactions in New York. Most machines require identity verification via phone number, government ID, or both.

Regulators are increasing scrutiny of bitcoin ATMs. Minnesota lawmakers introduced legislation to ban them in February 2026, and other states are considering similar measures. Reports of scams conducted through bitcoin ATMs have drawn attention from both federal and state law enforcement.

Bitcoin ATMs do not offer recurring buys, direct deposit, bill pay, Lightning Network support, or business accounts. Each visit is a standalone cash purchase.

Pros:

- Available for cash buyers without a bank account

- Immediate bitcoin delivery at the point of sale

- Hundreds of locations across New York for geographic accessibility

- No ongoing account relationship or digital platform needed. Each purchase is a standalone transaction

Cons:

- Total fees of 10%–25%+ make bitcoin ATMs the most expensive buying method by a wide margin

- No recurring buys, direct deposit, bill pay, or bitcoin withdrawal tools

- Exchange rate markups are not always disclosed, making true costs unclear

- No way to automate purchases or reduce fees with volume

Frequently Asked Questions About Buying Bitcoin in New York

Why are so many bitcoin platforms unavailable in New York?

The BitLicense and limited purpose trust charter require platforms to meet the strict custody, capital, cybersecurity, and compliance standards described above. About 36 entities have been approved under one of the two paths. Many companies choose to operate in states with lighter requirements rather than pursue either license.

Does it matter if a platform lists altcoins or prediction markets alongside bitcoin?

Platforms that list hundreds of altcoins and offer event contracts on sports and election outcomes generate revenue from trading volume and wagering activity across all of those products. Their product roadmap, support resources, and interface design reflect that breadth. Each new asset class or market pulls development further from bitcoin-specific tools. A platform built exclusively around bitcoin directs that investment toward features like bill pay, paycheck conversion, and automatic bitcoin withdrawals, services that only exist when bitcoin is the product, not one line item in a trading catalogue.

What is the lowest-cost way to buy bitcoin in New York?

Total cost depends on transaction size, frequency, and which fee tier you qualify for. Exchange platforms with advanced trading tiers charge as low as 0.20% per trade, and some platforms waive fees entirely on recurring purchases or direct deposit conversions. For regular buyers, fee waivers on automated purchases can reduce long-term costs more than a low per-trade rate on manual buys.

Do any platforms in New York support business accounts for bitcoin?

A few BitLicensed platforms offer business accounts, though availability and terms vary. Some limit which features are available to business clients. Others don't offer business accounts at all. If you're buying bitcoin for a company or as a self-employed individual, check whether the platform you're evaluating supports entity-level accounts before signing up.

Beyond buying and selling, what other bitcoin financial services are available in New York?

Some platforms available in New York go beyond a basic buy-and-sell interface with services like bitcoin-backed loans and line of credit, bill pay from bitcoin, fee-free paycheck-to-bitcoin conversion, free on-chain withdrawals, automatic withdrawals to your own wallet, and native Lightning for instant payments. Others offer direct deposit and auto-invest features. The range varies widely, and most platforms stop at buying and selling.

How to Choose a Bitcoin Platform in New York

- Product focus. Some platforms list bitcoin alongside hundreds of altcoins, prediction markets, and event contracts. Others skip altcoins entirely, though bitcoin may still share the app with stocks, payments, and other financial products. The product mix determines which features get built next.

- Bitcoin financial services beyond trading. Most platforms stop at buying and selling. A few offer bill pay from bitcoin, paycheck-to-bitcoin conversion, automatic withdrawals to your own wallet, and native Lightning payments. Those features only get built when bitcoin is the product, not one asset in a trading catalogue.

- Fee structure and transparency. Costs range from fee-free recurring buys to 25%+ at bitcoin ATMs. Some platforms post clear schedules. Others embed undisclosed spreads or use dynamic pricing that makes the true cost hard to know before you place an order. Over years of stacking, the gap between a platform that waives fees on automated purchases and one that charges 1–2% per transaction adds up to a meaningful amount of bitcoin.

The right platform depends on whether you're looking for a place to execute trades or a place to build your financial life around bitcoin.

This article is for informational purposes only and does not constitute financial advice, an endorsement, or a recommendation to use or avoid any product or service mentioned. All comparisons are based on publicly available information as of April 2026. Features, fees, and availability are subject to change. Readers should independently verify any claims before making financial decisions.

Zap Solutions, Inc. dba ‘Strike’ is licensed to engage in virtual currency business activity by the New York State Department of Financial Services. Bitcoin is not legal tender and is not backed by the government. Strike accounts are not FDIC-insured. Bitcoin’s price is volatile and can lead to losses. Sends on the Bitcoin network are irreversible, and losses from fraudulent or accidental transactions may not be recoverable.